Insurance by Industry

Insurance built for condo associations and their boards

From the master policy to directors and officers liability, Bittick helps associations in the Treasure Valley and beyond piece together coverage that actually fits how condo ownership works.

Condo building insurance is a group of related policies that a condominium owners association (COA) carries to protect the building structure, common areas, association finances, and board members from the liability exposures that come with shared ownership.

The coverage splits between the association and individual unit owners, and where one ends and the other begins depends on which of four master-policy structures the association chooses: bare walls, modified single entity, single entity, or full all-in coverage. Getting that structure right matters a lot, especially as associations in fast-growing Treasure Valley communities like Eagle and Meridian are managing newer, larger buildings where a gap in coverage can translate into a very expensive dispute.

Your condo association faces unique risks that need tailored protection.

From property damage to board member liability, we'll help you build a coverage plan that keeps your building and finances secure.

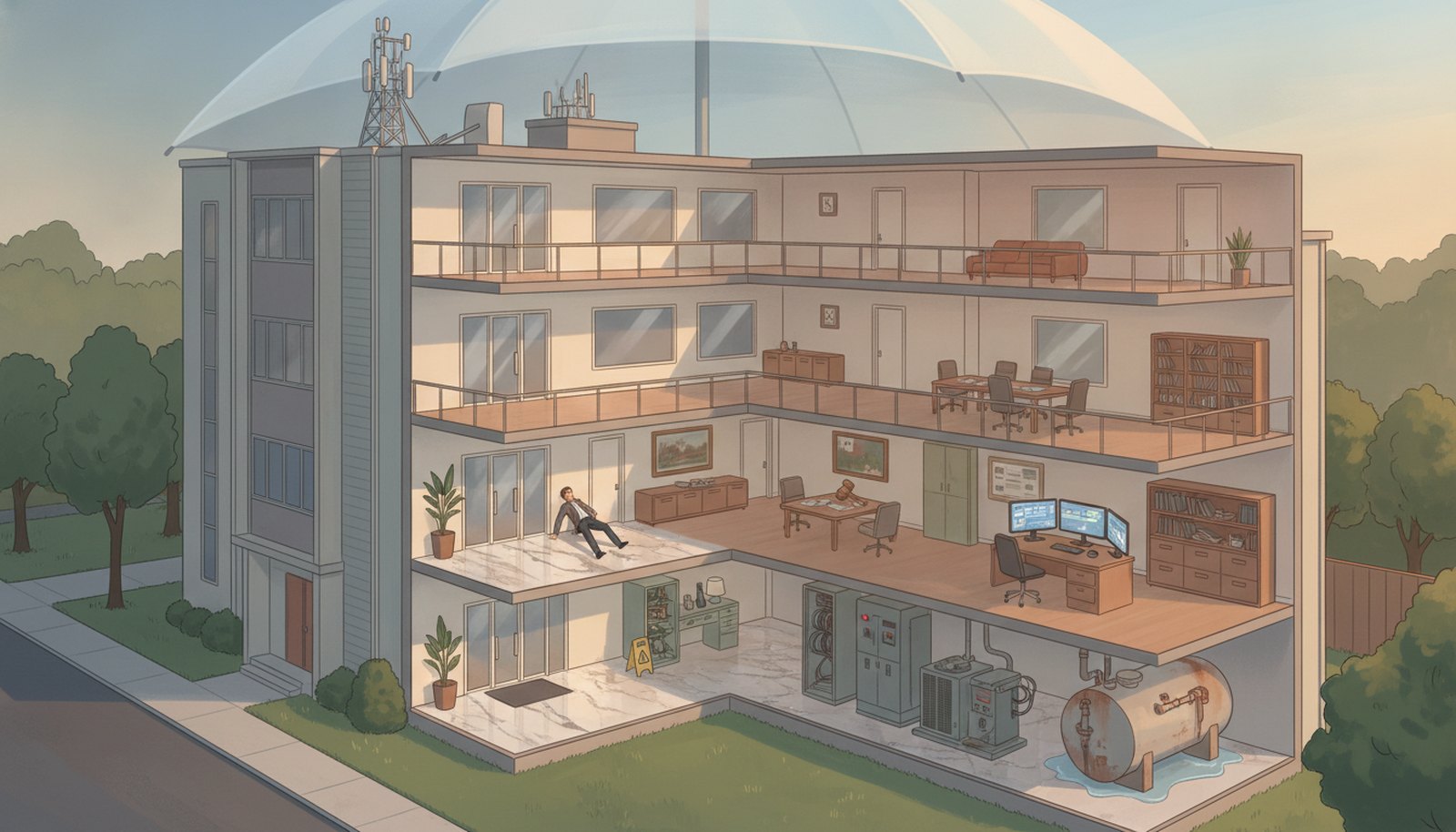

What this coverage includes

The association master policy (and its four structures)

The master policy is the foundation. It covers the building envelope and common areas — hallways, stairwells, elevators, parking areas, pools — against damage from fire, wind, and other covered causes. The four structures define how deep that coverage goes into each unit:

- Bare walls: The association covers walls, floors, and ceilings only. Unit owners cover everything inside.

- Modified single entity: Extends to original fixtures and appliances, but not upgrades or personal property.

- Single entity: Covers standard finishes like fitted kitchens, but owner upgrades may fall outside the policy.

- Full single entity (all-in): Covers original and upgraded fixtures, stopping at personal property.

Choosing the wrong structure — or failing to communicate it clearly to unit owners — is one of the most common and costly gaps Bittick sees in association portfolios.

Commercial property and general liability

Commercial property coverage pays to repair or rebuild after a covered loss and can include the association's own personal property and lost income if the building becomes temporarily uninhabitable. General liability covers the association when a third party is injured or their property is damaged on association-controlled ground. A visitor who falls in a parking lot, a contractor who claims property damage from work you directed, a neighbor whose fence was damaged by a tree in the common area — these are the kinds of claims that land on the association's general liability policy. Legal defense costs are included, which matters because even meritless lawsuits cost money to fight.

Directors and officers (D&O) liability

Board members make decisions: budget approvals, vendor contracts, rule enforcement, special assessments. Those decisions can generate lawsuits from unhappy unit owners, even when the board acted in good faith. Directors and officers liability insurance covers the legal costs to defend board members against covered claims and can fund any resulting judgments. Without it, individual board members may be personally exposed. This is one of the coverages Bittick most consistently flags as missing or underwritten when reviewing an association's existing program.

Crime, fidelity, and cyber liability

Associations collect dues, maintain reserve funds, and often employ or contract property managers who have access to those accounts. Crime and fidelity bond coverage protects against employee dishonesty, forgery, computer fraud, and fund theft by a board member or management firm. Cyber liability handles the other end of the digital risk: if resident data (payment information, personal records) is breached and the association is found liable, cyber coverage pays the fees, notification costs, and any resulting lawsuits. As associations shift more operations online, this exposure is growing.

Systems breakdown, umbrella, and environmental coverage

Systems breakdown coverage pays to repair or replace mechanical and electrical equipment — HVAC systems, elevator motors, boilers — after a mechanical failure. Standard property policies typically exclude mechanical breakdown, so this fills a real gap. A commercial umbrella policy sits above the general liability, D&O, auto liability, and employers liability policies to provide additional limits when a single large loss exhausts the underlying policy. Environmental coverage addresses a specific exclusion in most commercial property policies: pollutant cleanup. A leaking underground fuel tank, for example, generates cleanup costs and potential third-party lawsuits that the base policy will not touch.

Pairs well with

Commercial Property Insurance

Covers the physical building and association-owned personal property after a covered cause of loss. This is the spine of the master policy program and should be sized against current replacement cost, not original construction cost.

Learn more ›General Liability Insurance

Protects the association against third-party bodily injury and property damage claims arising from common areas. No association should operate without it.

Learn more ›Commercial Umbrella Insurance

Adds a layer of limits above the general liability, D&O, auto, and employers liability policies. Useful when a single large loss could exhaust the primary policy.

Learn more ›Cyber Liability Insurance

Covers data breach costs and resulting lawsuits if resident personal or financial information is compromised and the association bears liability.

Learn more ›Workers Compensation Insurance

Required in Idaho if the association employs maintenance staff or other workers directly. Covers medical expenses and lost wages for an employee injured on the job.

Learn more ›HO-6 Unit Owners Insurance

Individual unit owners need their own policy to cover personal property, interior improvements, and personal liability that the association master policy does not reach.

Learn more ›