Insurance by Industry

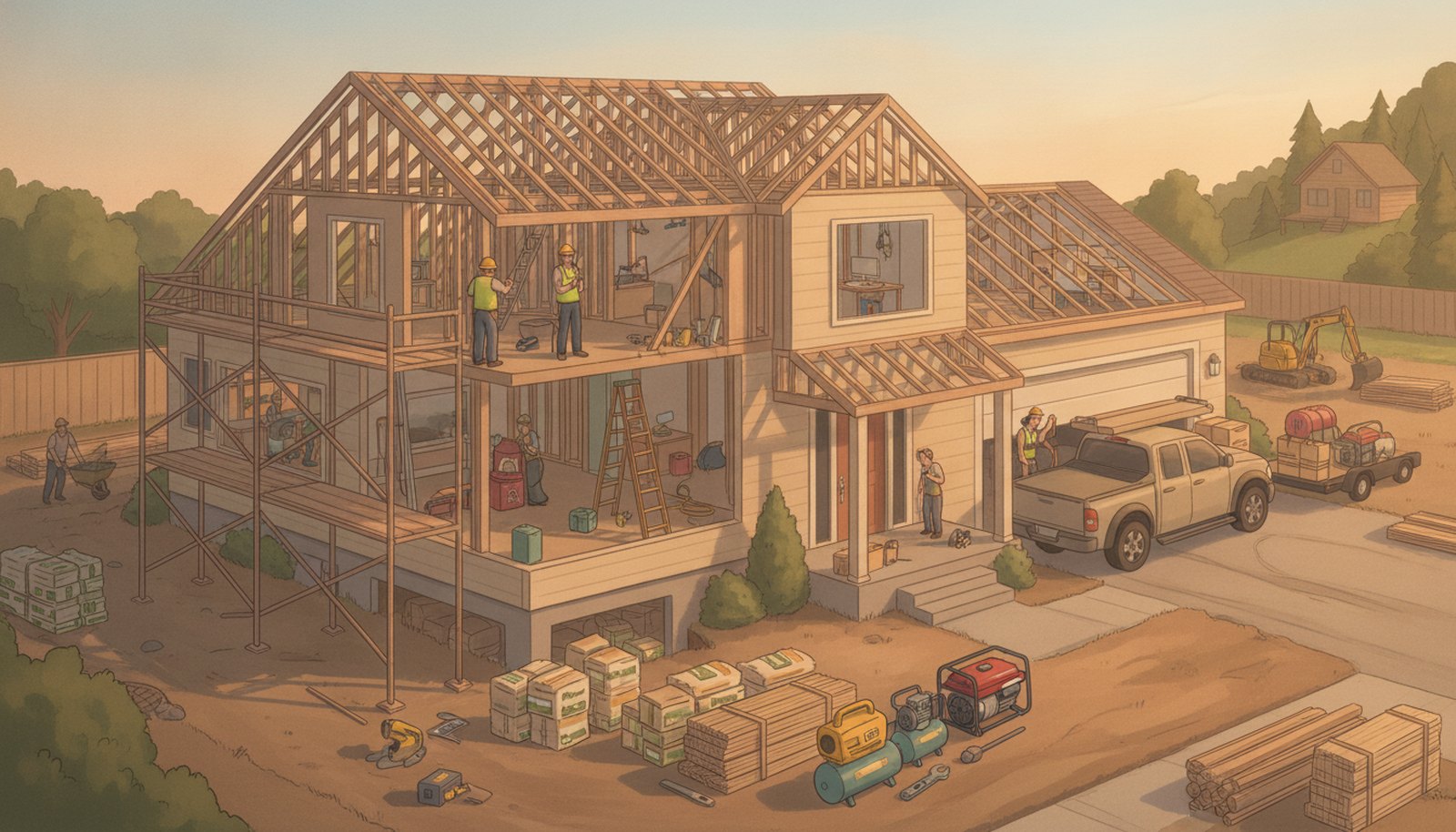

Contractor Insurance Built for Treasure Valley Trades

From a one-person finish crew in Eagle to a multi-trade GC running projects across the Boise metro, we shop the right coverage mix for your specific work.

Contractor insurance is a package of commercial policies that protects a contracting business against the liability, property, and workforce risks that come with doing physical work on other people's property. No single off-the-shelf policy covers everything a contractor faces, which is why most contractors carry several coordinated policies rather than one. At Bittick, we work with multiple carriers to build that package around what your trade actually does, not around a generic industry template.

The Treasure Valley's construction boom has put a lot of contractors on the road between Caldwell and the foothills above Eagle. That volume creates real exposure: tools moving between sites, subcontractors hired on short notice, project timelines disrupted by smoke-season delays or a hard freeze in November. The right coverage structure accounts for all of it.

Your contracting business faces unique risks that standard business insurance won't cover.

From job site theft to third-party liability, we help you build a protection plan tailored to how you work.

What this coverage includes

General Liability

General liability insurance covers bodily injury and property damage claims made against your business by third parties. If your crew damages a client's home, or a visitor trips over equipment on your site, general liability pays for legal defense and covered settlements. Most commercial clients and government contracts require proof of this coverage before you can bid, so it is often the first policy a contractor needs in place. It also extends to completed-operations claims, meaning a coverage trigger can happen after the job wraps if something you built or installed causes harm later.

Contractors' Equipment and Inland Marine

Contractors' equipment insurance covers your tools and machinery while they move between jobs. Standard commercial property insurance ties coverage to a fixed location; contractors' equipment coverage follows the gear. It responds to losses from theft, fire, vandalism, collision, and overturning, and many forms also cover flood and earthquake losses that property policies exclude. Inland marine is the broader category this falls under: it covers property in transit or at multiple locations. For a framing crew hauling a trailer of tools up Highway 55 every morning, this is the policy that actually responds when something goes wrong on the road or at the site.

Builders Risk and Installation Coverage

A building under construction is not a completed structure, so neither a standard property policy nor a homeowner's policy covers it. Builders risk insurance protects the structure and materials during the construction period, from groundbreaking through project completion. It covers materials stored at the site, materials in transit to the site, and the value of the partially finished structure itself. If lumber, generators, or copper pipe disappears from a Meridian townhome project overnight, builders risk is the policy designed to respond. Installation floaters extend similar protection to equipment that has been delivered but not yet permanently installed.

Commercial Auto

Personal auto policies exclude vehicles used for business purposes. Commercial auto insurance covers your owned or leased trucks, vans, and trailers when they are being used in the course of business, including coverage for bodily injury, property damage, collision, and comprehensive losses. A single at-fault accident in a work truck can generate a liability claim that far exceeds personal auto limits. If employees drive their own vehicles for work, hired and non-owned auto coverage fills that gap. Most contractor fleets need both.

Workers' Compensation

Idaho law requires workers' compensation coverage for most employers with one or more employees. It pays for medical treatment and lost wages when an employee is injured or becomes ill because of their job. For contractors, where work at height, with power tools, and in varying site conditions is routine, workers' comp is one of the most frequently triggered coverages in the policy stack. Carriers may offer experience-rated credits if your business maintains active safety programs and a clean loss history, which can meaningfully reduce your premium over time.

Pairs well with

Commercial Umbrella Insurance

General liability and commercial auto limits can be exhausted by a single serious claim in construction. A commercial umbrella policy sits above your primary policies and extends limits, typically from $2 million to $10 million, giving you a meaningful buffer if a large judgment or settlement exceeds your underlying coverage.

Learn more ›Commercial Property Insurance

If you own or lease office space, a shop, or a storage yard, commercial property insurance covers the building, equipment, inventory, and fixtures at that fixed location. It pairs with contractors' equipment coverage, which handles gear in transit, so your physical assets are protected wherever they are.

Learn more ›Business Owners Policy (BOP)

Smaller contracting operations sometimes qualify for a business owners policy, which bundles general liability and commercial property into one form at a lower combined premium than purchasing the two separately. A BOP is not right for every contractor, but it is worth evaluating if your operation is under a certain size threshold.

Learn more ›Surety Bonds

Many Idaho public contracts and some private clients require a contractor's license bond or a performance bond before work can begin. A bond is not insurance, but it signals to clients that you have financial backing if you fail to complete the work as contracted. We can help you understand when bonding is required and connect you with carriers that write them.

Employment Practices Liability Insurance (EPLI)

As your crew grows, so does the exposure to claims from current or former employees alleging wrongful termination, discrimination, or harassment. EPLI covers legal defense costs and settlements arising from those claims, which workers' compensation does not touch.