Insurance by Industry

Insurance Built for Houses of Worship

Your congregation is more than a building, and your coverage should reflect that.

Church insurance is a specialized form of business insurance that protects houses of worship against the specific risks that come with running a faith community: property damage, liability exposures, employment relationships, and the pastoral work your leaders do every day. A congregation is simultaneously a building owner, a community gathering space, an employer, and in many cases the home of a ministry leader, and a standard commercial policy rarely accounts for all of that. Bittick works with multiple carriers to find coverage that fits your church's actual operations, whether you run a small congregation in Eagle or a multi-campus ministry across the region.

Your church faces unique risks that standard business insurance may not cover.

From stained glass to staffing decisions, we help you protect your congregation and mission with coverage built for houses of worship.

What this coverage includes

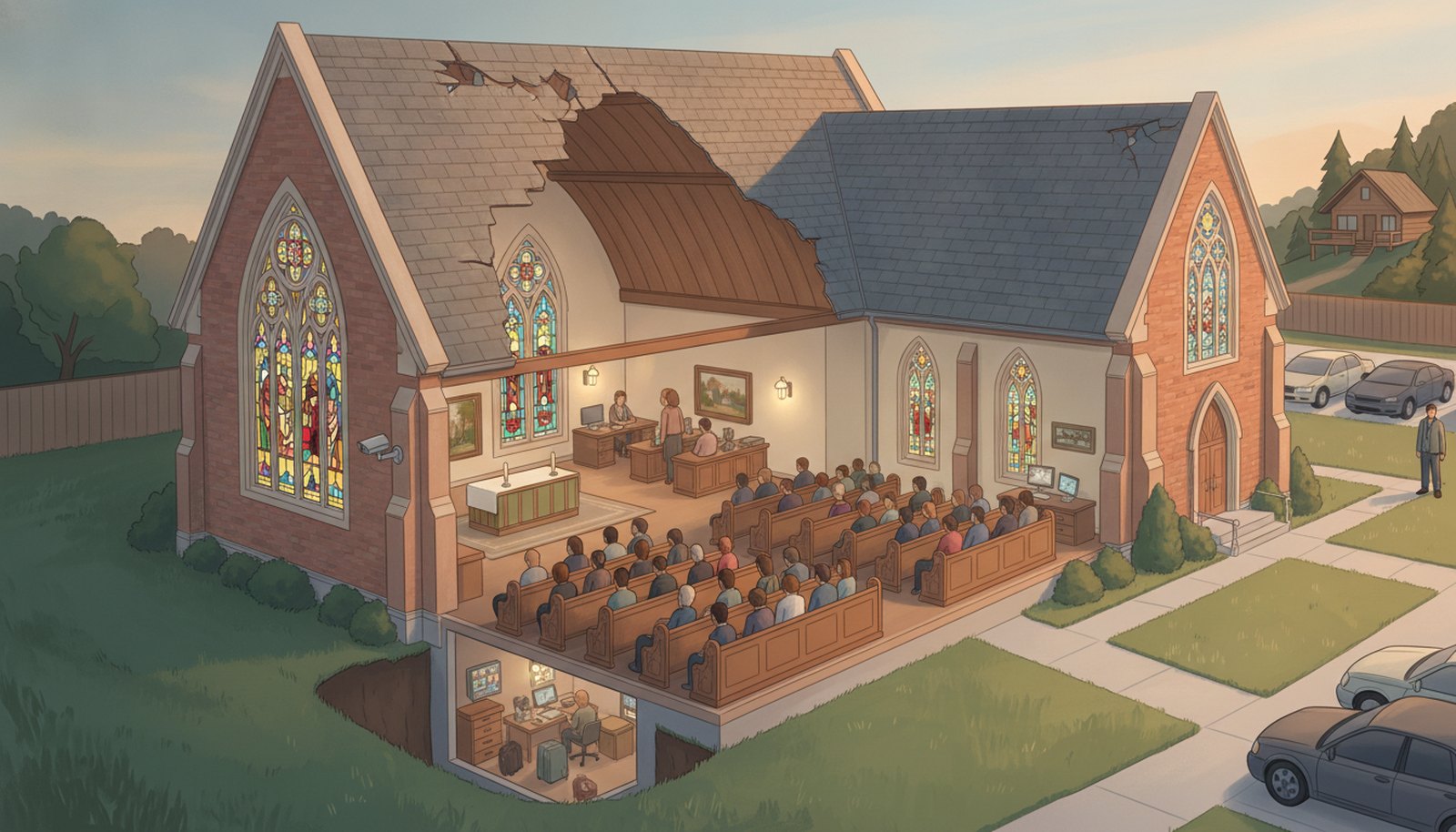

Property coverage for the building and its contents

Church property coverage pays to repair or rebuild after fire, wind, hail, vandalism, or theft. It also covers the contents inside, from audio-visual equipment and musical instruments to kitchen appliances used for community meals. One detail that matters here: when damage triggers a repair, local building codes may require upgrades to bring the structure up to current standards. A well-structured policy includes ordinance-or-law coverage so that compliance cost does not fall entirely on the congregation.

Stained glass and fine-arts coverage

Stained glass windows and other historic artwork can be worth hundreds of thousands of dollars, and replacing them is not a matter of calling the nearest glass shop. Carriers that specialize in church coverage can write the value of stained glass into the building limit or handle it under a fine-arts floater, depending on the piece. Either approach starts with a professional appraisal, which some policies cover. Getting that appraisal done before a loss is what makes the claim go smoothly afterward.

Liability coverage for the congregation and its leaders

General liability protects the church when a visitor slips on the steps, a vehicle damages property during an event, or an accident happens on the grounds. But churches also carry liability exposures that standard policies do not touch. Professional liability covers claims arising from pastoral counseling or statements made from the pulpit. Directors and officers (D&O) liability protects board members who make financial and operational decisions on behalf of the congregation. Religious freedom liability covers lawsuits stemming from closely held doctrinal positions. These are separate coverage lines, each addressing a distinct exposure.

Abuse and molestation liability

Abuse and molestation coverage addresses one of the most serious exposures a house of worship faces. Allegations against clergy, staff, or volunteers can result in significant legal costs regardless of outcome. This coverage funds the church's legal defense and, where liability is established, the resulting settlements. Carriers typically also want to see a written prevention policy and background-check procedures in place. Pairing the coverage with documented protocols is both a risk-management best practice and, with many carriers, a condition of getting the policy placed.

Hired and non-owned auto, mission travel, and other specialized coverages

When volunteers use personal vehicles to transport members or run errands for the church, the church shares in the auto liability exposure. Hired and non-owned auto coverage fills that gap. Churches that send teams on mission trips need travel liability coverage for those away-from-home exposures. Child-care operations, defibrillators and other safety equipment, the personal property of live-in ministry leaders, and key-person coverage for pastoral succession are additional lines worth reviewing based on how your congregation actually operates.

Pairs well with

Commercial Property Insurance

The structural foundation of any church policy. Covers the building, attached structures, and contents against fire, storm, theft, and vandalism, and can be written to replacement cost so you are not shortchanged at claim time.

Learn more ›General Liability Insurance

Covers third-party bodily injury and property damage claims on the church premises or arising from church activities. Essential for any congregation that opens its doors to the public.

Learn more ›Directors and Officers (D&O) Liability

Protects board members and church officers when decisions made on behalf of the congregation result in a lawsuit. Without it, individual volunteers on the board can be named personally in a suit.

Workers Compensation Insurance

Required in Idaho for most employers with one or more employees. Covers medical costs and lost wages if a paid staff member is injured on the job, whether that is a custodian, a childcare worker, or administrative staff.

Learn more ›Commercial Auto Insurance

Covers vehicles owned by the church, such as a shuttle van or bus used for transportation ministry. Pairs with hired and non-owned auto to close the gap when volunteers use personal vehicles.

Learn more ›Umbrella / Excess Liability Insurance

When a major liability claim exceeds the underlying policy limits, an umbrella policy picks up the difference. Churches that host large events or operate schools and daycare programs are particularly good candidates.

Learn more ›